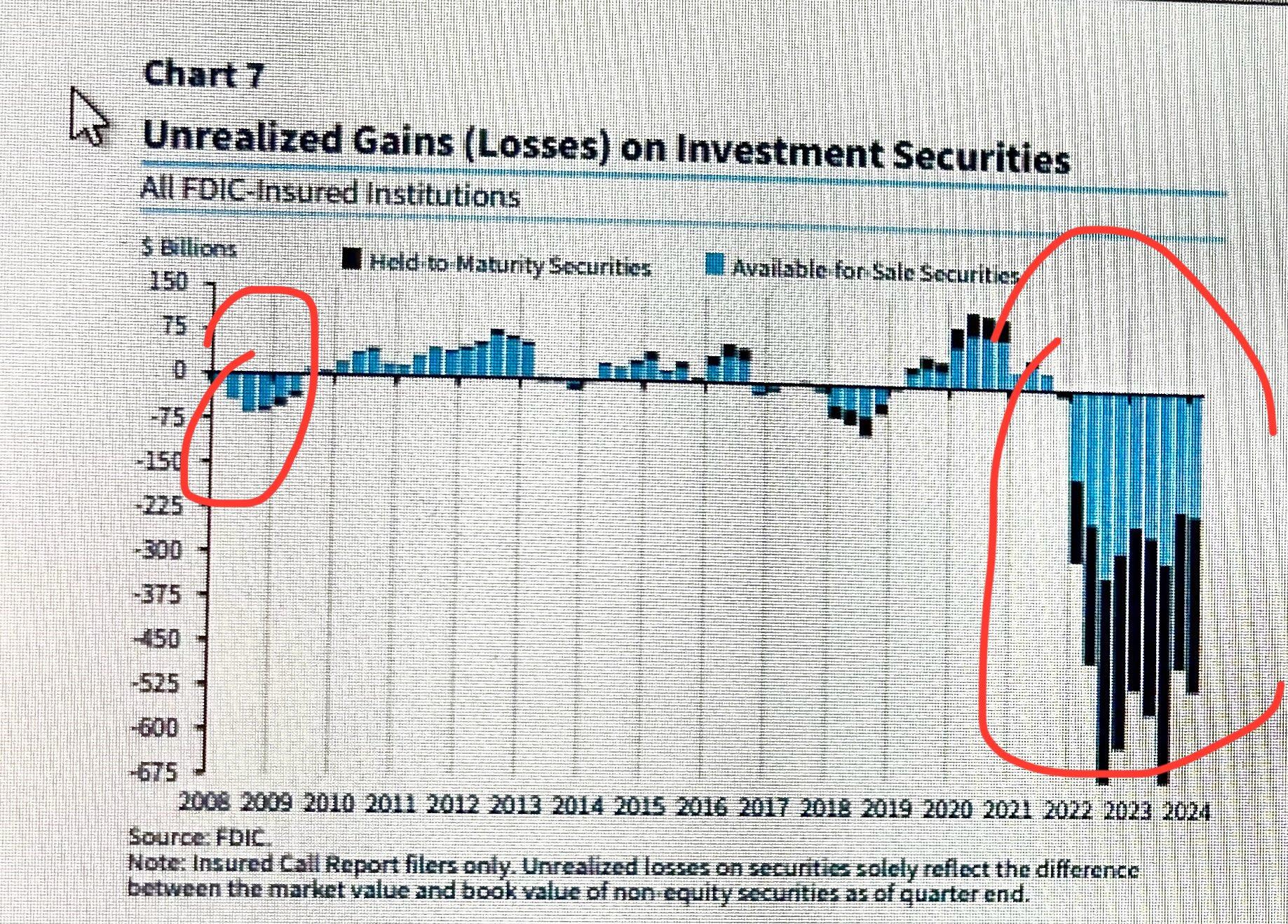

Say I would buy a security for 1000, and it price slumps to 750. As long as I do not sell the security no loss is incurred.

As a manner of bookkeeping requirement, the books have to be updated reflecting the current value or, worse, liquidation value, especially when a margin call is in the works.

The same with bonds. Say I would have a 1000 dollar bond yielding 3% a year. When the interest rate goes to 2, it means that my bond has become more valuable as the same amount of money yields more.

In case I wanted to get rid of the bond, I could earn a premium on it.

The opposite is true as well, Say the interest would go to 4. Who would be interested in getting a measly 3%? So, the acquiring price at a sale would be lower.

As we saw with these banks last year, the moment the securities are called in, that' s were the problem starts, cascading down in free fall.

Now consider the Bank of England in a state of REPO ANYTHING, including on-performing loans? And what about the ECB? They have a 2 trillion sword of Damocles above their heads.

The other thing about this graph is the size of the securities for sale ....So, what could be the reason to touché a loss? Some people really want out of the game....

{kind=link}

A waterfall?

Before reading further: activate this song by Leonard Cohen: You want it darker:

https://iyewtu.be/watch?v=hCXaPzEHPXY

Here it goes:

These are paper losses ....

Say I would buy a security for 1000, and it price slumps to 750. As long as I do not sell the security no loss is incurred.

As a manner of bookkeeping requirement, the books have to be updated reflecting the current value or, worse, liquidation value, especially when a margin call is in the works.

The same with bonds. Say I would have a 1000 dollar bond yielding 3% a year. When the interest rate goes to 2, it means that my bond has become more valuable as the same amount of money yields more.

In case I wanted to get rid of the bond, I could earn a premium on it.

The opposite is true as well, Say the interest would go to 4. Who would be interested in getting a measly 3%? So, the acquiring price at a sale would be lower.

As we saw with these banks last year, the moment the securities are called in, that' s were the problem starts, cascading down in free fall.

Now consider the Bank of England in a state of REPO ANYTHING, including on-performing loans? And what about the ECB? They have a 2 trillion sword of Damocles above their heads.

The other thing about this graph is the size of the securities for sale ....So, what could be the reason to touché a loss? Some people really want out of the game....

....Kill the flame

Nice analysis. The Leonard Cohen song made it really sink in.