Almost what sounds like needs to happen. We're going to be closing on a house after this deadline and I have better than a 740.

Penalize me for trying to do the best I can? That's absolute BS. Hoping that in the long term this will all be paid back, with interest and then some after lawsuits and settlements.

Agreed. Take a step back and think... is any of this real? The shit they come out with daily wouldn't fly 3 years ago. The Anon in me thinks most of this is bs to rattle the sleeping normies to wake the fk up. I could be wrong. The ability of so called intelligent humans to tolerate complete incompetence is even blowing my mind, lol. It's like they workshop at the alter of Harlon's Razor.

Ask your realtor about it, maybe if you got your loan approved before this starts, it won't be added onto your mortgage. Come back after you close on your house and let us know if they added that fee onto your mortgage.

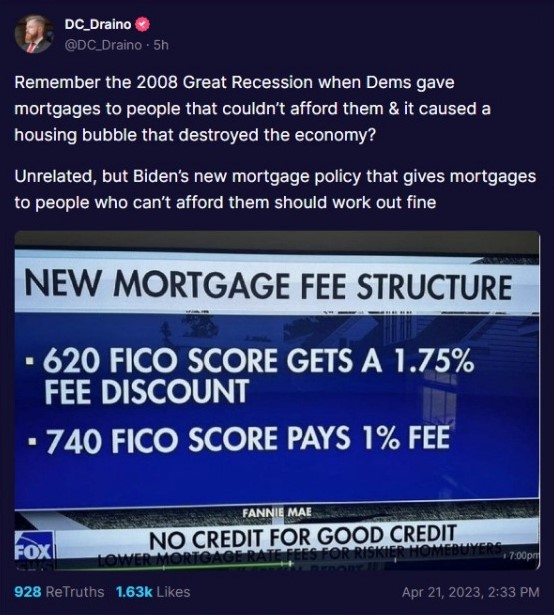

While the info in the media is not exactly accurate (is it ever)?) it is true that the recent changes to LLPA’s (loan level pricing adjustments - which have always existed but recently modified), were done in an attempt to allow more people to qualify. They never learn! The original LLPA’s were mostly based on national statistics on defaults, slow pays, etc. That makes more sense! Higher risk loans pay higher rates. Not anymore :(

Remember that an important part of the Great Reset is stealing all the land and forcing all the people into SMART15-minute cities, which are essentially prisons without walls.

This is one of the ways to steal land from people. The banks give someone a loan even though the bank knows the borrower will eventually default on said loan. Then the bank gets to keep the property.

In fairness, there were a whole lot of Republicans that were in on the "you get a mortgage and you get a mortgage and you get a mortgage!" game back in the mid 2000's before the collapse.

Also in fairness, the new mortgage structure is far crazier to the point of absurdity than what they were doing back then. This new plan is literally mortgage welfare.

They don’t care because the “money” is invented out of thin air. They get interest payments on money they never had in the first place. This is a ploy to get that last few dollars out before the SHTF.

I learned about this in the mid-late 80’s. I watched Mellon Mortgage foreclose on entire portfolios. I thought then (still do) that it was a huge land grab. Nothing else makes sense.

While flying in a balloon, I shot holes in in to see what would happen. It fell to the ground and I almost died! So now I got another balloon and am flying high! I think I'll shoot holes in it to see if that happens again! (Our government in action)

Shit, I should forget to pay several bills for two months then apply for a loan. Yeah, this should work out great!

Almost what sounds like needs to happen. We're going to be closing on a house after this deadline and I have better than a 740.

Penalize me for trying to do the best I can? That's absolute BS. Hoping that in the long term this will all be paid back, with interest and then some after lawsuits and settlements.

Agreed. Take a step back and think... is any of this real? The shit they come out with daily wouldn't fly 3 years ago. The Anon in me thinks most of this is bs to rattle the sleeping normies to wake the fk up. I could be wrong. The ability of so called intelligent humans to tolerate complete incompetence is even blowing my mind, lol. It's like they workshop at the alter of Harlon's Razor.

Ask your realtor about it, maybe if you got your loan approved before this starts, it won't be added onto your mortgage. Come back after you close on your house and let us know if they added that fee onto your mortgage.

New construction, will finish later than May 1st. Kinda different than conventional home purchase.

Nothing is ever paid back. Lawsuits should be filed.

What could possibly go wrong? Yikes! What nitwit dreamt this up?

While the info in the media is not exactly accurate (is it ever)?) it is true that the recent changes to LLPA’s (loan level pricing adjustments - which have always existed but recently modified), were done in an attempt to allow more people to qualify. They never learn! The original LLPA’s were mostly based on national statistics on defaults, slow pays, etc. That makes more sense! Higher risk loans pay higher rates. Not anymore :(

Remember that an important part of the Great Reset is stealing all the land and forcing all the people into SMART15-minute cities, which are essentially prisons without walls.

This is one of the ways to steal land from people. The banks give someone a loan even though the bank knows the borrower will eventually default on said loan. Then the bank gets to keep the property.

In fairness, there were a whole lot of Republicans that were in on the "you get a mortgage and you get a mortgage and you get a mortgage!" game back in the mid 2000's before the collapse.

Also in fairness, the new mortgage structure is far crazier to the point of absurdity than what they were doing back then. This new plan is literally mortgage welfare.

They don’t care because the “money” is invented out of thin air. They get interest payments on money they never had in the first place. This is a ploy to get that last few dollars out before the SHTF.

I learned about this in the mid-late 80’s. I watched Mellon Mortgage foreclose on entire portfolios. I thought then (still do) that it was a huge land grab. Nothing else makes sense.

Makes me all the more happy I paid off my mortgage several years ago.

While flying in a balloon, I shot holes in in to see what would happen. It fell to the ground and I almost died! So now I got another balloon and am flying high! I think I'll shoot holes in it to see if that happens again! (Our government in action)

Riddle me this: what happens if the government pays people to stop smoking?

Answer that correctly and you know exactly what will happen here.

Here come the high risk mortgage startups again. Had some friends go from

DC Draino's TS post - https://truthsocial.com/@DC_Draino/posts/110238472283342045