It is called "force majeure." Acts outside the scope of normal living conditions.

Now, consider the things that have been going on the past few years and what many here suspect might be planned for the near future, try to think like an attorney (if it does not cause brain damange, which it might), and re-read that last paragraph:

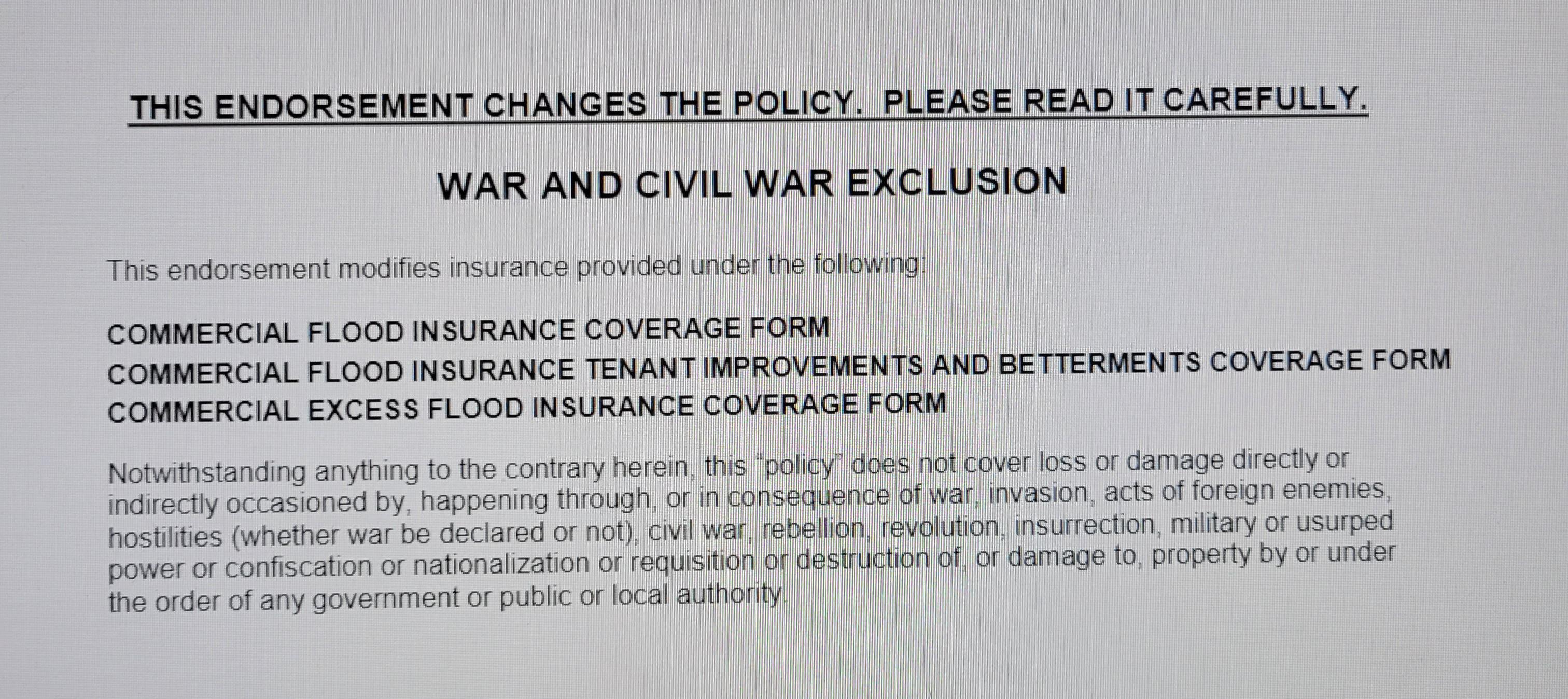

Notwithstanding anything to the contrary herein ..."

Translation: If any of this shit happens, you are f*cked. Your insurance "policy" is not worth the paper it is printed on.

... war, invasion, acts of foreign enemies or hostilities (whether war be declared or not), civil war, rebellion, revoluation, insurrection, military or usurped power, or confiscation or nationalization ...

Who will decide if this policy should be ignored due to any of these things? The insurance company will, and then you will have to sue to prove they are wrong (assuming courts are functioning).

A couple of thoughts:

"acts of foreign enemies" -- like election theft? Like bioweapon "plandemic?"

"insurrection" -- like wandering through a tour of the Capitol Building?

"usurped power" -- like election theft and the installation of a president via fraud?

"confiscation or nationalization" -- like if a communist takeover happens, and you suddenly "own nothing, and like it?"

If we do not have Rule of Law, then we have nothing. ALL contracts would terminate due to force majeure, potentially, and it would be massive chaos.

Yep. That's what we're doing now. In 2015 our S. FL our Homeowners was $1200. In 2017 it went up to $2200. In 2020 it went up to $3800. Before we moved last year I got the renewal and it was going to be $5000 and it was going to be cancelled at the end of the year to be picked up by Citizens. A common occurrence down there. Sold that place, bought our new one cash. Screw the insurance companies. One of the biggest scams going besides taxation.

Which is why I and many others are prepared to pay off the balance on a home if need be. This is how they are going to take away home ownership from people through a backdoor methods via unrealistic demands from home insurance companies.

You’re so right ,, they raised the rates so high in Cali , many went without , then the fires came , burned them out and they had no ins , they had to sell their burnt land , pennys on the dollar , my friend retired from San Diego school district , being patriots they wanted to get out of liberal land and go up north. They built 3 homes on their 54 acre in berry creek , nor cal , for her and husband and two of their kids and grand kids . It was totally free and clear , they spent years paying it off after building and then they moved to their dream retirement . They lost everything. Nusellini wouldn’t even let the fire fighters try to stop the fires . Within days the vultures were in town grabbing everyone’s property .

Insurance and rent culture is also a way they dictate business policy.

If every business must rent, then every business must buy insurance. If every business must buy insurance, then business policy can be controlled through insurance.

Think theft policy. Think guns in buildings. Ties back to insurance.

Whoa man.....that seems a bit extreme don't you think? Rates across the board have gone through the roof but not having home insurance seems hella risky....

Insurance companies were not paying claims on policies due to the fires? I know the gov check wasn't shit but did not hear about insurance companies stiffing home owners who had HO policies.

It’s risky but if you honestly look in the numbers how many homes actually burn down or are destroyed by storms if you are in a safe stable area (not hurricane, tornado alley, etc.)

Statistically you should be more than fine. However homeowner insurance can also helps save you from other liability like fall injuries if I’m not mistaken

Yeah, you have to fight for every penny owed after something that is covered, dont ever sign paperwork without a lawyer after say a house fire or they will screw you over big time. We had house fire and thankfully I was too upset to sign anything on the evening it happened (and they certainly did try to get me to sign, I just kept refusing) and because of that, we got the best we could out of it in the end instead of the crap they wanted to give us. If they can get away with not giving you back money for your losses they will use it they tried very hard to blame it on the kid playing with lighter since they found a lighter up on top of our entertainment center (where a 5yrld could not even reach if he tried and he was terrified of lighters anyway), ended up it was one of those stupid stand up lamps, bulb blew and caught couch on fire but, even finding the real cause was a pain for us, we had to keep insisting to keep looking. It was crazy.

Of course insurance likes your dollar payments increasing while their coverage decreases. Although it is a normal exclusion, it would be interesting to see what changed and caused them to inform you of the modification.

I notice that there also is no definition listed here. But .... it is easy to see how rebellion, acts of foreign enemies ( maybe ask them if this concern Israel?), invasion and requisition can play together: open borders.

{kind=link}

It is called "force majeure." Acts outside the scope of normal living conditions.

Now, consider the things that have been going on the past few years and what many here suspect might be planned for the near future, try to think like an attorney (if it does not cause brain damange, which it might), and re-read that last paragraph:

Translation: If any of this shit happens, you are f*cked. Your insurance "policy" is not worth the paper it is printed on.

Who will decide if this policy should be ignored due to any of these things? The insurance company will, and then you will have to sue to prove they are wrong (assuming courts are functioning).

A couple of thoughts:

"acts of foreign enemies" -- like election theft? Like bioweapon "plandemic?"

"insurrection" -- like wandering through a tour of the Capitol Building?

"usurped power" -- like election theft and the installation of a president via fraud?

"confiscation or nationalization" -- like if a communist takeover happens, and you suddenly "own nothing, and like it?"

If we do not have Rule of Law, then we have nothing. ALL contracts would terminate due to force majeure, potentially, and it would be massive chaos.

^^^

Standard exclusion. Been around a while.

Second that. Last major change was the addition of terrorism after 9/11.

Yeah, this is why I cancelled my home insurance. Wayyyy too many exceptions. Better to pocket the cash and have your own rainy day fund.

Yep. That's what we're doing now. In 2015 our S. FL our Homeowners was $1200. In 2017 it went up to $2200. In 2020 it went up to $3800. Before we moved last year I got the renewal and it was going to be $5000 and it was going to be cancelled at the end of the year to be picked up by Citizens. A common occurrence down there. Sold that place, bought our new one cash. Screw the insurance companies. One of the biggest scams going besides taxation.

You can just cancel your homeowners' insurance? Do you have to own your home outright, first?

Yup.

Which is why I and many others are prepared to pay off the balance on a home if need be. This is how they are going to take away home ownership from people through a backdoor methods via unrealistic demands from home insurance companies.

You’re so right ,, they raised the rates so high in Cali , many went without , then the fires came , burned them out and they had no ins , they had to sell their burnt land , pennys on the dollar , my friend retired from San Diego school district , being patriots they wanted to get out of liberal land and go up north. They built 3 homes on their 54 acre in berry creek , nor cal , for her and husband and two of their kids and grand kids . It was totally free and clear , they spent years paying it off after building and then they moved to their dream retirement . They lost everything. Nusellini wouldn’t even let the fire fighters try to stop the fires . Within days the vultures were in town grabbing everyone’s property .

Insurance and rent culture is also a way they dictate business policy.

If every business must rent, then every business must buy insurance. If every business must buy insurance, then business policy can be controlled through insurance.

Think theft policy. Think guns in buildings. Ties back to insurance.

Whoa man.....that seems a bit extreme don't you think? Rates across the board have gone through the roof but not having home insurance seems hella risky....

How well did it work out for the folks in Hawaii who had insurance?

They got $700 so there's that

They ain't get that $700 from their insurance though. 🤣🤣

Insurance companies were not paying claims on policies due to the fires? I know the gov check wasn't shit but did not hear about insurance companies stiffing home owners who had HO policies.

https://greatawakening.win/p/17rTBKlIiU/interesting-new-lahaina-damage-v/

Iirc it's mentioned near the end of the video.

A bit of trust me bro but it's all the info I have. Link back here if you find anything better.

No worries and will do....thanks for the link merf.....

No kidding

It’s risky but if you honestly look in the numbers how many homes actually burn down or are destroyed by storms if you are in a safe stable area (not hurricane, tornado alley, etc.)

Statistically you should be more than fine. However homeowner insurance can also helps save you from other liability like fall injuries if I’m not mistaken

Buying a lottery ticket may have the same chances of delivering as your homeowners insurance does.

Yeah, you have to fight for every penny owed after something that is covered, dont ever sign paperwork without a lawyer after say a house fire or they will screw you over big time. We had house fire and thankfully I was too upset to sign anything on the evening it happened (and they certainly did try to get me to sign, I just kept refusing) and because of that, we got the best we could out of it in the end instead of the crap they wanted to give us. If they can get away with not giving you back money for your losses they will use it they tried very hard to blame it on the kid playing with lighter since they found a lighter up on top of our entertainment center (where a 5yrld could not even reach if he tried and he was terrified of lighters anyway), ended up it was one of those stupid stand up lamps, bulb blew and caught couch on fire but, even finding the real cause was a pain for us, we had to keep insisting to keep looking. It was crazy.

All mine from forever had those exclusions.

Weird that it was added to the flooding sections. I wonder if folks down stream of a big dam should think?

So would they classify ANTIFA riot damage as war by a foreign enemy? Civil unrest would be the big one I’d worry about.

Of course insurance likes your dollar payments increasing while their coverage decreases. Although it is a normal exclusion, it would be interesting to see what changed and caused them to inform you of the modification.

I notice that there also is no definition listed here. But .... it is easy to see how rebellion, acts of foreign enemies ( maybe ask them if this concern Israel?), invasion and requisition can play together: open borders.

Show the policy provider. Anyone can type that shit up and post it.